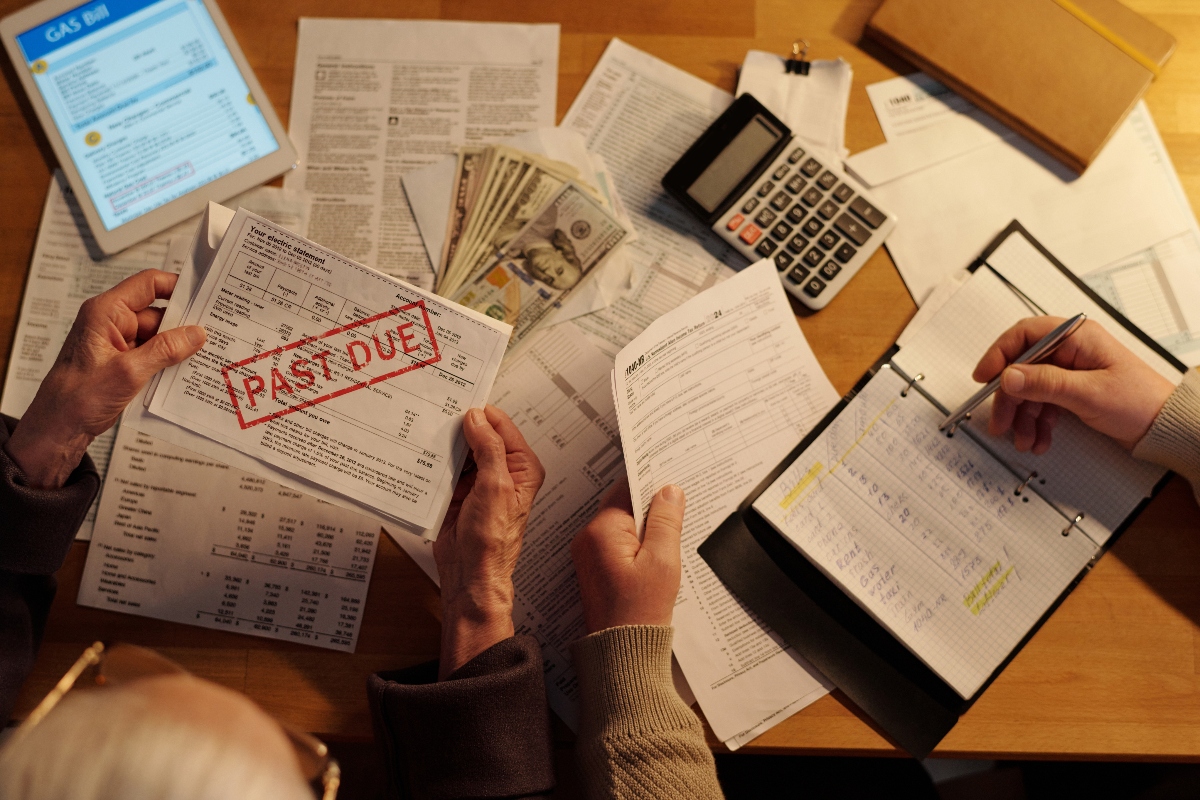

Credit is the key that opens doors to financial opportunities in the United States, says Experian, one of the most recognized credit bureaus. For the Hispanic community, a good credit score not only makes it easier to buy a house or a car, but also influences interest rates, access to loans and even job opportunities.

According to the Consumer Financial Protection Bureau (CFPB), a credit score below 670 can mean paying thousands of dollars extra in interest. That’s money that could be in your pocket! The good news is that improving your credit score is possible with clear and effective steps. QueOnnda.com presents a practical, expert-backed guide for you to take control of your financial history and move toward your goals.

1. Check your credit report

Before you can improve your credit score, you need to know where you stand.

You can get one free report a year at AnnualCreditReport.com, recommended by the Federal Trade Commission (FTC).

Identify errors and report them immediately – a small mistake could be costing you a lot!

2. Pay on time, every time

Payment history accounts for 35% of your credit score, according to FICO.

Set reminders or set up automatic payments.

Even one late payment can reduce your score drastically. Remember: punctuality pays, big time.

Improving your credit score is possible with clear and effective steps

QueOnnda.com

3. Reduce your credit usage

Keep your credit utilization below 30%.

For example, if your limit is $1,000, try to use less than $300.

According to Experian, reducing this percentage can have an immediate positive impact on your credit score.

4. Do not open too many accounts

Each application generates an inquiry that may temporarily lower your credit score.

According to Equifax, opening multiple accounts in a short period of time is a risky signal to lenders.

Apply for credit only when you really need it.

5. Keep open accounts

Length of credit history accounts for 15% of the score, says FICO.

If you have old cards with no balance, keep them open. This shows financial stability and responsibility.

Buzzy

Improving your credit score is not a luxury, it’s a necessity.

With information backed by FICO, Experian and the CFPB, you have tools and strategies at your fingertips to increase your financial score.

Good credit opens doors – from lower interest rates to greater economic opportunities.